How To Get Cash From Your Home Equity

The traditional refinance

For many people, especially those who bought homes in late 2022 or after, the mortgage market hasn’t changed much in terms of loan pricing, so to access cash from the equity your have in your home, the easiest path might be to do what’s called a “cash out refinance”. With a cash out refinance, you can access the equity in your home (up to 80% of your home’s current value, for most refinance programs) and receive funds at the time your loan closes. A new loan, with the new loan balance, takes the place of the former loan, so you’re left with one loan.

When it makes the most sense

A traditional cash out refinance makes sense for most people if you’re keeping the interest rate on your loan similar, or lower, than the loan being replaced. It may also be the best option if you fit program guidelines that are specific to more traditional mortgages (for example, if you have average or below average credit scores, an FHA cash out loan may be a better option than a HELOC or alternative option). It can also make sense regardless of your current loan rate if you’re using the cash to consolidate higher rate or higher payment debt.

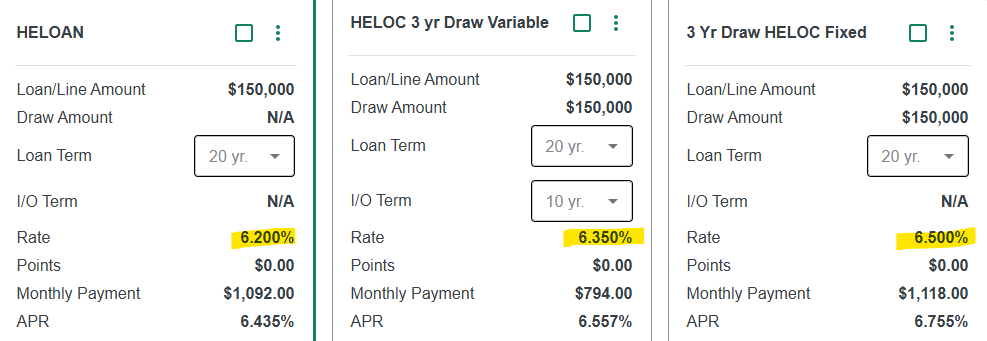

The HELOC

HELOC (Home equity line of credit) loans are very popular at the moment, primarily because millions of Americans are feeling “locked in” to the mortgage rates they were able to secure in 2020-2021, when rates were at historic lows. It’s a tough pill to swallow to trade a rate in the 3s for a rate in the 6s (though it can make sense, depending on what you’re using the money for – we can do a free analysis to see which options are best!), so many opt to take out a HELOC as a 2nd mortgage.

HELOCs offer some nice benefits over traditional refinances – typically, you can borrow up to 90% of your home’s value (sometimes more!), and many HELOC programs allow for interest-only payment options (so you can pay the loan down in larger installments at your own pace, with smaller mandatory monthly payments). Many HELOCs are tied to the ‘prime rate’, so rates can go up or down based on economic circumstances. Typically these rate movements are incremental over time, so the risk is low for rates to spike suddenly.

The easiest way to think of a HELOC is that it’s like a credit card using your home as collateral – you get a line of credit, and a “draw” – that is, the amount you borrow and use when you open the line. You can continue to draw and repay the balances on the account, making payments only on the amount you have borrowed as a draw at a given time.

When it makes the most sense

The HELOC is optimal for someone that has a very low rate first mortgage in place and wants to access (and re-access) cash from their equity for a 3-10 year period. The optimal borrower is disciplined in repayment and can afford to pay back the loan in chunks while using the interest-only minimum payment to maximize their cashflow. They need money, but maybe don’t need all of it right now, or aren’t sure what they’ll need (you can open a HELOC with a large line of credit but you only pay on the “draw”, or what you have borrowed from the line at a given time).

The HELOAN

A HELOAN is similar to a HELOC in that it’s usually used as a 2nd lien, going behind an existing first mortgage, with the difference being that the HELOAN is not a line of credit, but a one time loan giving a borrower funds in a lump sum that are repaid in a traditional amortization schedule. For example, a 30 year HELOAN would provide a lump sum to a borrower in the amount of the loan minus closing costs, and payments would be spread equally over 360 payments.

When it makes the most sense

The HELOAN is a great product for the person that doesn’t want to touch their first mortgage and has a pretty good idea on how much money they need, and they need it in a lump sum soon. They get their money, can repay it at a fixed rate and the payments are on a regular payment schedule – no different from most fixed rate first lien mortgages.

Takeaways

All of these products have a place in the overall housing and mortgage market, and used in the right circumstances, can help homeowners improve their financial wellbeing. HELOCs and HELOANs are available with a wide variety of terms (for very well qualified borrowers, terms can be extremely attractive, but rates can climb quickly for less qualified applicants), but typically carry rates slightly higher than first mortgages.

Home renovations, debt consolidation, cash for investment property down payments (or cash purchases) are some of the more common uses for these products, but anyone needing to access equity in their home can apply.

Have questions about HELOCs, HELOANs, or refinance options?: Ask an expert here!

Want a quote to see what options look like for your unique circumstances?: Get a quote here – free & fast!